Natixis Global Asset Management recently published a white paper, Can the Federal Reserve Be Replaced by a Mathematical Formula?, highlighting the Fed Oversight Reform and Modernization act approved by the Financial Services Committee of the House of Representatives. This Act would require the Fed to establish a mathematical formula in setting interest rate policy. Not surprisingly, the Fed is not in favor of this type of proposal.

Several highlights in the Natixis paper:

- The positive side is that it could force the Federal Reserve to monitor developments that it has completely overlooked in the past: credit, asset prices, liquidity, external deficit; it would then need a more complex formula than a Taylor rule;

- One negative side is obviously that a mathematical formula cannot take into account the complexity of an economic situation: dozens of variables would have to be included (real growth, labour costs, longterm interest rates, savings rate, detailed situation of the labour and real estate markets, etc.);

- Another negative side is that in contemporary economies, central banks have - and will probably increasingly have - instruments other than the short-term interest rate: purchases and sales of financial assets (bonds, ABS), quantitative easing when interest rates become zero, banks’ prudential ratios, etc. Should each instrument be determined by a mathematical formula?

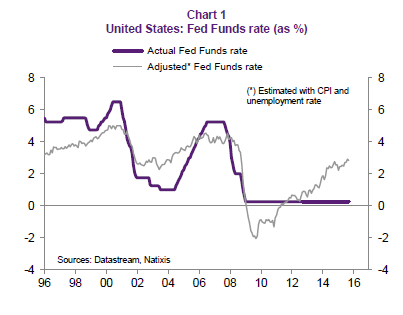

- This plan will in all likelihood be abandoned. However, we should not forget that the Federal Reserve’s choices, not guided by a mathematical formula, have quite often been catastrophic over the past 20 years (by accepting asset price bubbles, external deficits, excessive debt levels, etc.). Automating these choices would not have only drawbacks.

|

| From The Blog of HORAN Capital Advisors |

The paper notes that today the Fed uses other monetary tools other than adjustments to short term interest rates:

"purchases or sales of financial assets, generally as part of a quantitative easing programme; in the future, increasingly, banks’ prudential ratios (capital ratios, required reserves, etc.). This makes it possible to markedly increase the effectiveness of monetary policy compared with a situation where only the short-term interest rate is controlled, especially by also controlling long-term interest rates"

"By freely setting monetary policy over the past 20 years without being constrained by the use of a mathematical formula, the Federal Reserve has let the following appear:

"A more complex mathematical formula than a Taylor rule could have forced the Federal Reserve to react to these developments and to not let excessive indebtedness and asset price bubbles develop, which led to the subsequent financial and banking crises."

- A huge US external deficit from 2002 to 2008;

- Recurrently, excessive private-sector debt levels;

- Asset price bubbles;

- Useless excess liquidity.

"But we should not forget that a complex formula that takes into account credit, asset prices, external deficits, etc. would prevent the errors of judgement and monetary policy choices that for the last 20 years have led to - particularly in the United States - crises linked to excessive indebtedness and bursting asset price bubbles."

Source:

Can the Federal Reserve be replaced by a mathematical formula?

Natixis Global Asset Management

By: Patrick Artus

November 27, 2015

No comments :

Post a Comment